Oracle’s debt-fueled transformation

Capital allocation, customer base, and investment merits

For much of early 2026, Oracle ORCL 0.00%↑ was a stock in purgatory. Shares cratered nearly 60% from their September 2025 highs, weighed down by a bruising combination: a $50 billion AI expansion plan that spooked investors, a revenue miss, and whispers that its landmark OpenAI data center buildout was behind schedule and underfunded. The 52-week low came early April at $134.57.

Then, almost imperceptibly, something shifted; over the next eight weeks, Oracle rose more than 80%.

Early May: the company closed $16 billion in financing for a Michigan data center. It landed a classified Pentagon AI contract. Jim Cramer name-dropped Oracle as a market tell, pointing to a $553 billion contracted backlog — a number up 325% year-over-year — as evidence of AI demand so overwhelming that Oracle itself said it could “comfortably meet and likely exceed” its targets. JPMorgan initiated with an Overweight. The stock was at $180.

Then Snowflake reported. Then Atlassian. Then Dell. Each earnings beat from an enterprise software peer was another data point that the AI infrastructure thesis wasn’t hype — it was real, it was accelerating, and Oracle sat near the center of it. Capital that piled into AI hardware names for two years began rotating, looking for the picks-and-shovels plays that hadn’t yet repriced. Oracle’s OCI cloud infrastructure — growing at 84% year-over-year — suddenly looked like one of the most underappreciated assets in technology.

By late May, the market profile told the story. The value area, that band of heaviest trading activity between roughly $139 and $194, became a launchpad. Each time Oracle touched the upper boundary and pulled back, buyers returned. The 50-day moving average, still trailing at $174, was left behind.

The crescendo came on June 1st. Jensen Huang took the stage at Computex and told the world that AI was “an opportunity, not a threat” for software companies. Oracle announced Project Jupiter — a sprawling AI data center campus in New Mexico. The stock surged nearly 10% to $248, capping what iShares’ software ETF recorded as the sector’s best month since 2001. Larry Ellison’s net worth cleared $300 billion. The ascent that had begun in the shadows was suddenly front-page news.

By June 3rd, shares sat at $230, pulling back modestly as options markets priced in double-digit volatility around the June 10th earnings report. Analysts had been lifting targets for weeks — UBS to $285, BNP Paribas to $283, Scotiabank to $290. The consensus Moderate Buy with a ~$261 average target that had looked ambitious in February now looked almost conservative.

The bears had their arguments: $124 billion in long-term debt, negative free cash flow projected through 2028, and an uncomfortable concentration of risk in a single customer — OpenAI representing roughly 54% of the backlog. Oracle was, as the skeptics noted, building a mountain of AI infrastructure on borrowed money and borrowed time.

But the chart told a different story. From $134 to $248 in roughly two months, mostly in silence, mostly before the headlines caught up. A mature software company, 47 years old, threaded itself into the spine of the AI economy — and the market had only just started to notice. The June 10th earnings report looms as the next inflection point — either the validation of everything the past six weeks have promised, or the moment the market asks for proof.

Either way, the quiet part of this story is over.

Oracle is no longer the sleepy enterprise database incumbent of the prior decade. It has transformed into a high-growth, high-leverage AI infrastructure play—and the debt is the engine.

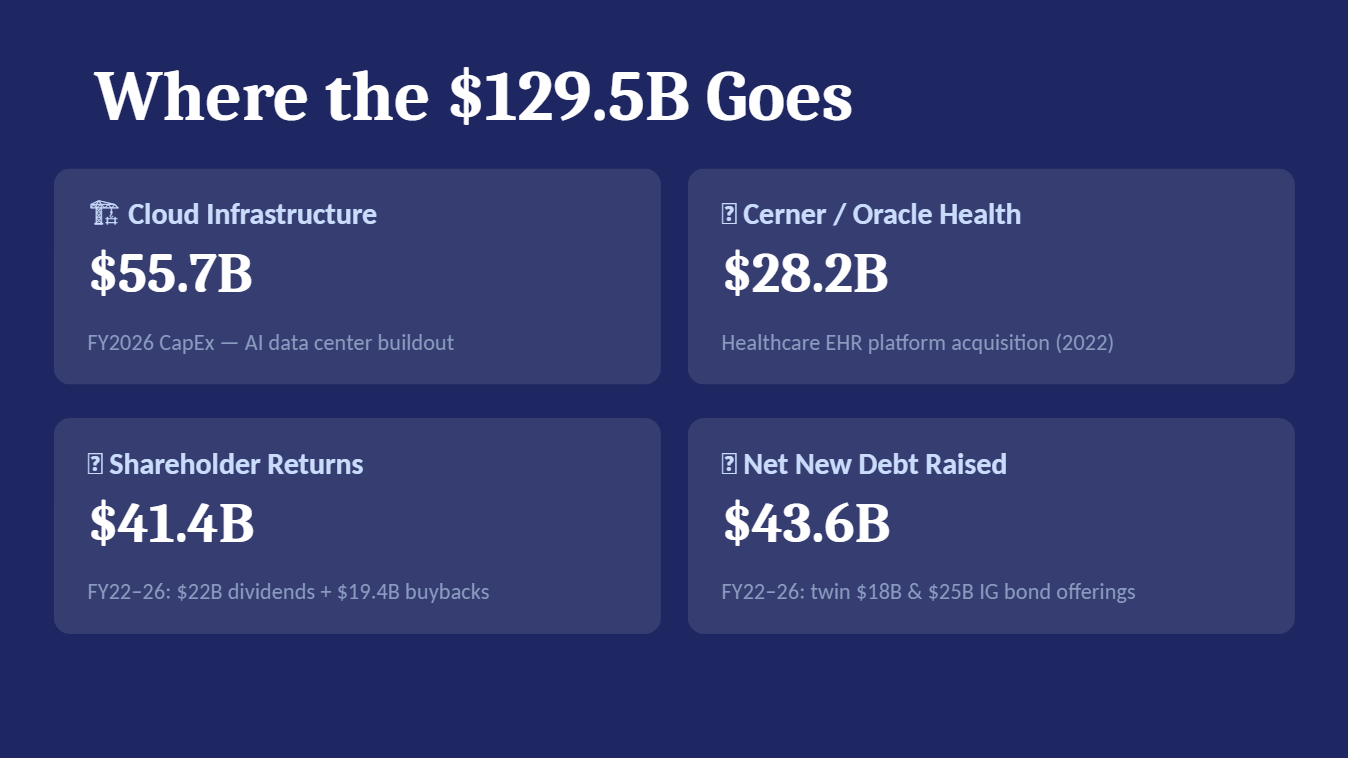

The $129.5 billion in total debt on Oracle’s balance sheet as of May 31, 2026 doesn’t represent financial distress. It represents a deliberate, aggressive capital deployment strategy across four distinct buckets.

Cloud Infrastructure: The $55.7 Billion Bet

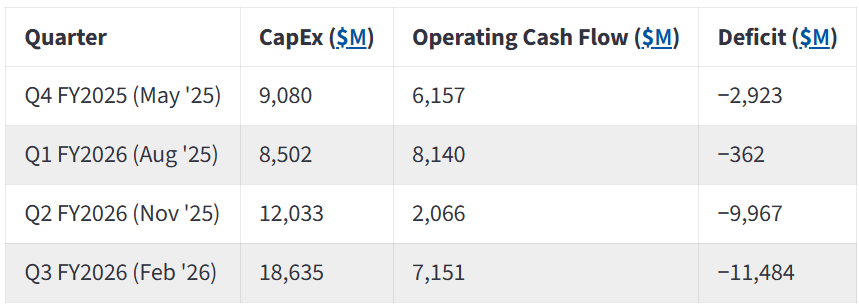

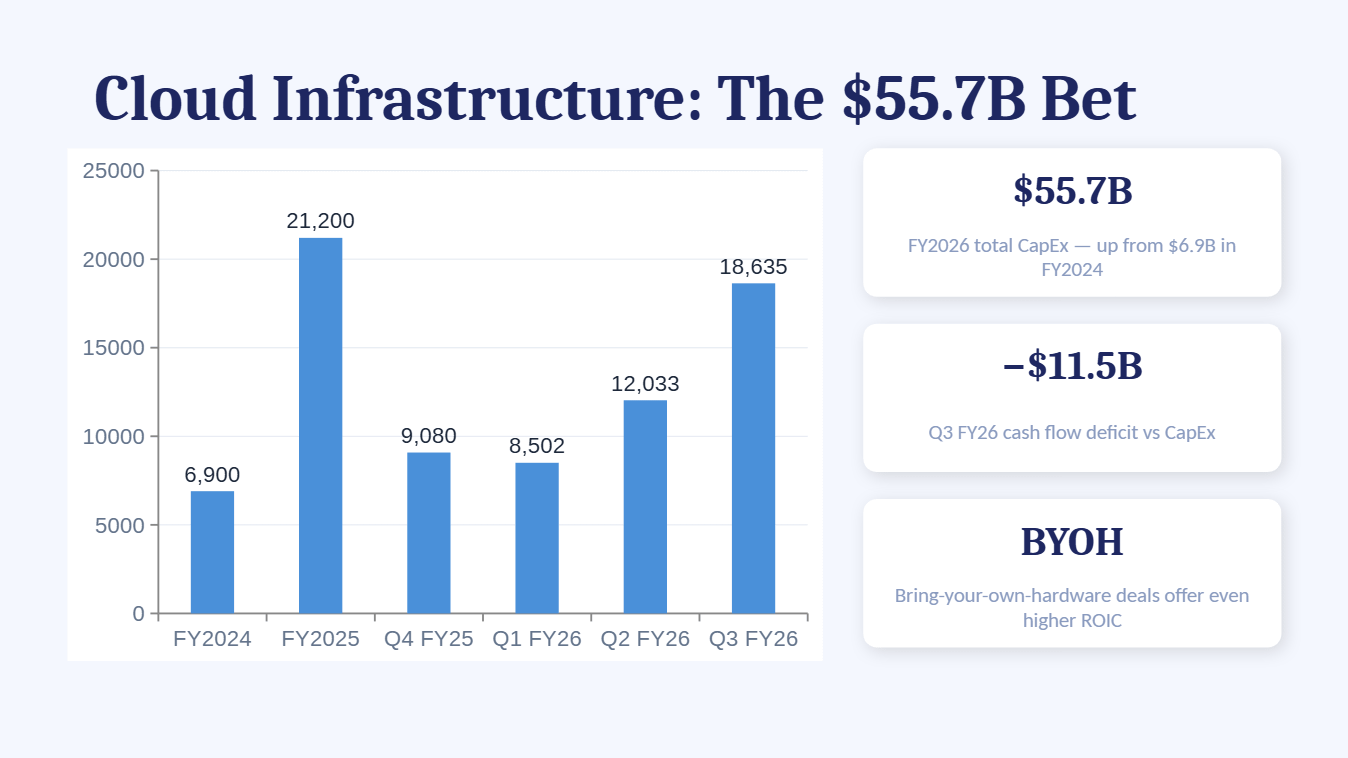

Oracle’s fiscal 2026 capital expenditures reached $55.7 billion—a figure that dwarfs the $21.2 billion spent in FY2025 and the $6.9 billion in FY2024. The quarterly trajectory tells the acceleration story with precision:

Oracle is building data centers as fast as construction timelines and power procurement allow. Each facility is purpose-built for AI training and inference workloads, with a distinctive architectural advantage: Oracle’s networking fabric interconnects tens of thousands of GPUs with latency characteristics that rival or exceed the hyperscalers. Management guided to “high-20s percent” returns on invested capital at steady state, with bring-your-own-hardware arrangements delivering even higher ROIC.

The CFO disclosed that $48 billion in net cash capex was deployed in FY2026—approximately $8 billion above the reported number when accounting for prepayments and timing effects. This is not maintenance capex. This is greenfield construction.

The Cerner Acquisition: $28.2 Billion for Healthcare

Oracle closed the Cerner acquisition on June 8, 2022 for $28.2 billion. This was not a vanity purchase. Oracle Health—the rebranded Cerner unit—gives Oracle ownership of electronic health record infrastructure inside thousands of hospital systems. The strategic logic is multilayered: clinical data is among the most valuable training corpora for healthcare AI models, and Cerner’s installed base provides distribution for Oracle’s autonomous database and cloud services into a vertical with extraordinary regulatory stickiness.

Oracle Health is expected to return to double-digit growth in FY2027 as the Cerner EHR platform is rebuilt into an AI-native version. The rebuild is expensive and multi-year, but the end state—an AI-augmented clinical workflow system running on OCI—has no direct analog among the hyperscalers.

Capital Returns: $41.4 Billion to Shareholders

Over FY2022–FY2026, Oracle returned approximately $41.4 billion to shareholders—$19.4 billion in share repurchases and $22.0 billion in dividends. The repurchase pace decelerated sharply as capex demands escalated: from $16.2 billion in FY2022 to just $0.1 billion in FY2026. Dividends, conversely, grew every year—from $3.5 billion to $5.8 billion—and represent a $23.2 billion annualized commitment that Oracle’s board is unlikely to cut.

The Net Debt Bridge: $43.6 Billion in Five Years

Total net debt issuance across FY2022–FY2026 reached $43.6 billion. The largest slug came in FY2026 at $39.2 billion—twin $18 billion and $25 billion investment-grade bond offerings that funded the data center buildout. Long-term debt on the balance sheet rose from $85.3 billion in May 2025 to $124.7 billion by February 2026. Short-term debt sits at $9.9 billion. The interest expense line is climbing in lockstep: $978 million, $923 million, $1,057 million, and $1,180 million over the last four reported quarters, respectively

The customer base has bifurcated into two distinct cohorts: the legacy enterprise base and the new AI-native hyperscale buyers.

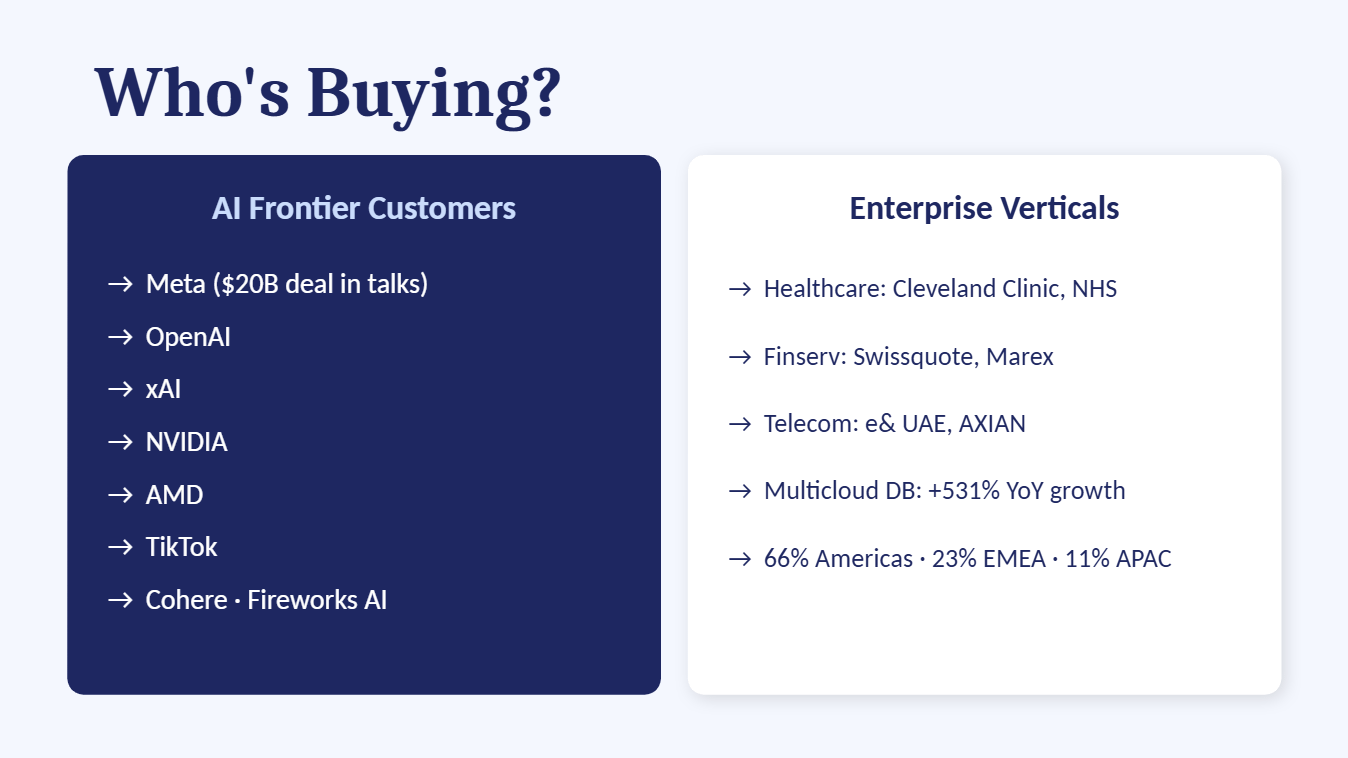

The AI Infrastructure Buyers

Oracle’s most strategically significant customer commitments were disclosed in the February 2026 financing plan: AMD, Meta, NVIDIA, OpenAI, TikTok, and xAI. These are not customers buying a few database licenses. These are AI frontier labs and platform companies signing multi-year, multi-billion-dollar infrastructure consumption contracts. Reuters and DCD reported Meta was in talks for a $20 billion Oracle cloud deal. The concentration is real, but so is the revenue visibility: these contracts feed directly into the $638 billion remaining performance obligation (RPO) balance.

Beyond the headline names, Oracle has landed a constellation of AI-native startups: Cohere, Fireworks AI, Applied Intuition, SoundHound, and Anthrogen. These smaller wins matter because they represent the next generation of AI workload demand—companies that may scale from millions to hundreds of millions in annual cloud spend

The Multicloud Database Strategy

Oracle’s most underappreciated customer story is its multi-cloud database business. Customers can now run Oracle Database services natively inside AWS, Azure, and Google Cloud without re-architecting applications. Multi-cloud database revenue grew 531% year-over-year in Q3 FY2026. This is not a rounding error—it is a structural shift in how enterprises consume Oracle’s most valuable intellectual property. The Gartner and IDC language Oracle cites emphasizes that no other database vendor offers this portability across all three major hyperscalers.

Enterprise Verticals

Healthcare customers include Cleveland Clinic, Monash Health, and NHS Shared Business Services. Financial services wins include Bank of N.T. Butterfield, Fibabanka, National Bank of Fujairah, Marex, Swissquote, and Groupama. Telecom deployments span Yas (AXIAN Telecom) and e& UAE. The geographic revenue split runs 66% Americas, 23% EMEA, and 11% Asia Pacific—a distribution that provides some insulation from any single region’s economic cycle

The Growth Case Is Exceptional

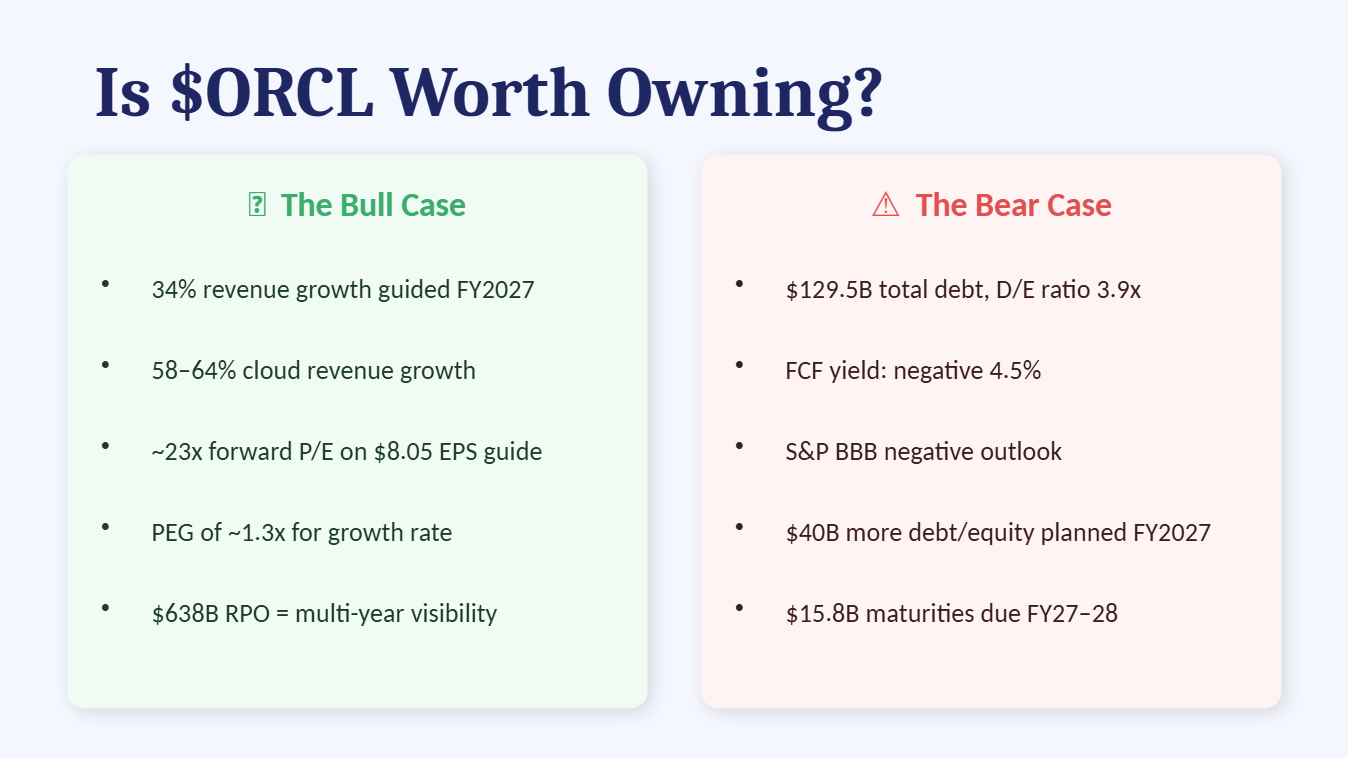

Oracle guided FY2027 total revenue growth of 34% in constant currency. Q1 FY2027 revenue is expected between 27% and 29% in dollars. Cloud revenue is projected to grow 58% to 64%. Non-GAAP EPS guidance of $8.05 implies 18% growth in constant currency after stripping one-time investment gains. The $638 billion RPO—up 363%—provides multi-year revenue visibility that few companies in any sector can match. At $184.29, the stock trades at approximately 22.9x forward earnings on management’s $8.05 guide, and 23.9x on consensus $7.71.

[Inference] For a company guiding 34% revenue growth with a PEG ratio of 1.3x, that forward multiple is defensible—even attractive—relative to the growth rate. The problem is that the P/E and PEG are calculated on earnings that exclude the capital cost of the growth itself.

The Financing Burden Is Also Exceptional

Oracle plans to raise an additional $40 billion in debt and equity during FY2027. This includes a $20 billion at-the-market equity issuance already announced—representing roughly 3.8% dilution at current market capitalization. The company carries $129.5 billion in total debt against $38.5 billion in common shareholders’ equity, producing a debt-to-equity ratio of 3.9x. Net debt stands at approximately $97.6 billion, or 2.7x EBITDA of $36.5 billion. Free cash flow yield is negative 4.5%.

The credit rating agencies have taken notice. S&P rates Oracle BBB with a negative outlook. Moody’s assigns Baa2, also with a negative outlook. Fitch holds BBB with a stable outlook. These are investment-grade ratings, but they sit two to three notches above non-investment grade. A downgrade would increase Oracle’s cost of refinancing at precisely the moment its maturity wall demands attention: approximately $15.8 billion comes due across FY2027–FY2028.

Interest expense is compounding. The quarterly run rate has reached $1.18 billion and will rise as the full weight of the FY2026 issuances flows through the income statement. At 9.2x interest coverage, Oracle has room—but not infinite room. If the Fed delivers the 1.0 to 1.5 hikes priced between October and year-end 2026, floating-rate exposure (approximately $4.3 billion in commercial paper and floating notes) adds roughly $40–$50 million in annual interest per 100 basis points. The larger impact is refinancing risk: rolling $15.8 billion at coupons 100 basis points higher adds roughly $158 million in annualized interest.

The Verdict

Oracle is not a “good” or “bad” stock in the abstract. It is a highly specific bet on AI infrastructure demand growth outpacing the cost of financing that growth. The bull case requires OCI revenue to continue compounding at 70%+ annually, multicloud database to maintain triple-digit growth, and Oracle Health to deliver on its AI-native EHR rebuild—all while the company navigates $40 billion in incremental capital raises without triggering a credit downgrade or a funding crisis.

The bear case requires only one thing to go wrong: a slowdown in AI infrastructure demand that leaves Oracle holding $55 billion-plus in annual capex commitments against decelerating revenue. In that scenario, the leverage that amplified the upside becomes a structural liability.

For a portfolio already concentrated in technology and facing a hawkish Fed under Kevin Warsh—who has explicitly prioritized price stability and removed forward guidance—Oracle’s debt profile introduces a dimension of risk that extends well beyond the standard growth-stock multiple-compression trade. The stock makes sense as a conviction position only if the investor has underwritten the $638 billion RPO, believes in management’s ROIC assumptions, and is prepared for the volatility that accompanies a company funding its own transformation at this scale and this speed.

Improving financial outcomes by boosting financial literacy.

If you enjoyed this newsletter…

Refer a friend.

Or a family member—or even a stranger—as long as they open up our emails and keep us out of their spam folder.

But wait! There’s more…

Give your friend (or relative) the gift of a premium subscription—even just for one month—and we’ll comp your subscription for 6 months.

YES, you can game the system!

How to game the system:

Click the link above, pay for one month to a new subscriber’s email

Cancel within 30 days

Seven months for the price of one: you get 6 months, your friend gets 1.

And if you refer two friends: you get a whole year free.

Of course, we would prefer you not cancel right away… so instead, tell your friend to game the system too.

Pay it forward and we all win

One free subscriber turns into 3 premium subscribers—with a total of 14 premium months between the three of you.

That’s an 85% discount to the best newsletter user experience in investing.